1st April 2019 was a historic date for India as the country’s maiden Real Estate Investment Trust (REIT) was listed on the bourses. The euphoria on Dalal Street was evident with investors placing 181 million bids and the issue being oversubscribed by 2.6 times. On the day of listing, the scrip closed at Rs 314.10 per unit, up 4.7% from its issue price of INR 300 — vouchsafing that investors whole-heartedly welcomed REITs in India.

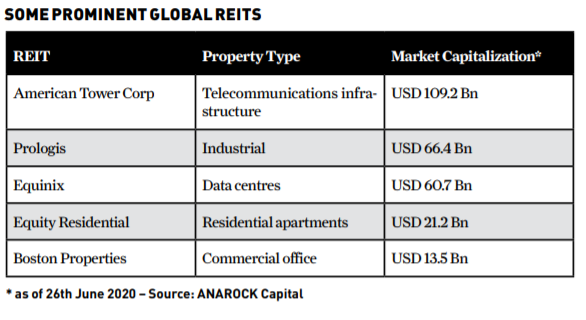

REITs were introduced in India only recently, and currently focus only on commercial offices. However, they have existed globally for around 60 years. Across the world, some of the largest REITs own property types such as telecommunication infrastructure, industrial (distribution centres, warehouses, etc.), data centres, retail malls, healthcare facilities, commercial offices, residential projects and several other assets.

As of August 2019, the US REITs market capitalization was 96% of the real estate market while in Singapore and Japan, it was 55% and 51%, respectively.

In comparison, in India it was only 17% as of August 2019. Despite the markets being in a turmoil over the past several months – further exacerbated by the COVID-19 outbreak which impacted businesses and stock markets alike – the REIT market opportunity is still significant and also still largely untapped in India.

The India Story

SEBI introduced draft rules, partnered with several stakeholders, and enacted the REIT regulations in 2014. Between 2014 and 2016, the rules were revised several times to address concerns, primarily related to double taxation.

In 2014, the sponsors were given a tax deferral to transfer the shares of the Special Purpose Vehicle (SPV) to business trusts in consideration for units. Taxation was deferred until the sale of units. In 2015, minimum alternate tax (MAT) deferral was also introduced.

In 2016, the dividend distribution tax (DDT) exemption was provided at the SPV level. The fact that this makes the REIT taxable in the hands of the shareholders has caused some concern – but SEBI, along with industry stakeholders, is working to sort this out as well. The regulator has been instrumental in the success of the REIT vehicle in India, crafting a robust process and efficient mechanism to ensure transparency and generate interest from institutional investors.

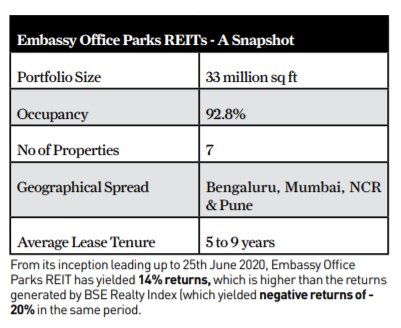

Presently, Embassy Office Parks REITs is the only publicly-traded REIT in India and as of 26th June 2020, its market capitalization was around USD 3.45 Bn (17% of the listed real estate stocks’ market capitalization in India).

India REITs Market: Underexplored, Opportunities Galore

India’s maiden REIT has paved the way for many others to follow suit. We are witnessing consolidation of portfolios and good quality office assets are exchanging hands. Several developers and owners of commercial office real estate are in various stages of preparing for the listing. Considering that the Indian office sector is quite organized and has the presence of corporate developers, it opened the way for the maiden REIT.

However, the COVID-19 outbreak has slowed down activity, with global investors carefully watching the emerging WFH trend that may shrink office space requirements. Developers worry about the attainable rental values for renewals and new leases, as there may be a demand slowdown in the short term. Commitments on future spaces, if withdrawn, may adversely impact the commercial office sector.

Currently, the top 7 cities of India have close to 550 million sq ft Grade A office supply, of which 310 – 320 million sq. ft. is REIT-able. Indian REITs are still at a nascent stage with immense potential even in other asset classes going forward.

• 43 million sq ft of Grade A mall spaces sized more than 2 lakh sq. ft., excluding stand-alone anchors, have been added across the top 7 cities of India in the last decade. These malls, with an overall occupancy of more than 80%, can potentially provide a major retail REIT opportunity. Much depends on how the COVID-19 situation evolves

• As of 2019, 110 million sq ft Grade A warehousing stock existed across India.

• If the residential rental housing market in India gets further organized, it is capable of emerging as a sizeable opportunity for residential REITs. Considering that residential constitutes around 80% of the India real estate market, there is a huge opportunity to systematically develop rental housing and enable the formation of residential REITs.

In addition to the above traditional asset classes, India is a booming market for ‘new-age’ asset classes such as student housing, co-living and senior living which have inherent potential to be developed as REITs, albeit it appears to be several years away as of now.

To Sum it up

The successful listing of Embassy Office Parks REIT was a major step in the right direction. The realization of a larger REIT market in India will hinge on the further benefits that markets offer to investors. With regards to capital gains tax concerns, India could consider taking cues from mature markets such as the UK (which has exempted REITs from income and gains tax.)

With another realty major K. Raheja Corp now gearing up to announce their REIT listing, India is better positioned than ever before and there is considerable incentive for making the proposition even more attractive. With the right kinds of evolutionary steps, India can join the elite club of global REITs. Establishing and nurturing such investment vehicles helps unlock the massive value of real estate assets and enable retail participation in the development of the nation.

Shobhit Agarwal is Managing Director & CEO – ANAROCK Capital