On 12th December 2022, in a written reply to the Lok Sabha, the Minister of State for Finance Pankaj Chaudhary said that the Reserve Bank of India (RBI)’s Central Bank Digital Currency (CBDC) pilot in the retail segment has underlying technology backed by the widely used blockchain technology and has several common features with physical cash. He added that the CBDC will not earn any interest but can be converted into bank deposits.

The rise of digital transactions and an increasing shift from cash to online modes have bared users and the banking system to fraud. While new forms of digital transactions such as Unified Payments Interface (UPI) are backed by the government and have several security features, cryptocurrency, which has gained relevance in the past few years, sits entirely out of regulated structures. Increasing use of cryptocurrencies has also led to an increase in individuals falling prey to scams, illicit transactions being done with these digital forms of currencies, and has led to the opening of doors for use of government-backed digital currencies such as the digital rupee.

After having called for a complete ban on the use of cryptocurrencies in India, the launch of the Digital Rupee in pilot form for Wholesale segment (e₹-W) on 1st November 2022, and for retail digital Rupee (e₹-R) on 1st December 2022 is an initiative by the RBI which not only offers alternatives to cryptos but also introduces an additional form of digital payment systems, especially given the increasing usage of digital payments across the country.

Easing Payments, Countering Counterfeit

The Digital Rupee will be transacted using wallets backed by blockchain technology making the payments final, thereby reducing settlement risk. It is freely convertible against physical currency and can be used interchangeably but does not require a user to have a bank account as in the case of other forms of digital transactions such as UPI. Moreover, unlike private cryptocurrencies, the Digital Rupee or any type of central bank digital currency is regulated by the central bank. According to RBI’s concept note on the Digital Rupee released in October 2022, the e-rupee will help ‘bolster India’s digital economy, enhance financial inclusion and make the monetary and payment systems more efficient’. More importantly, it is expected to help reduce costs associated with physical cash management and boost cross-border transactions and contribute to easing the bank cash management, currently a herculean task.

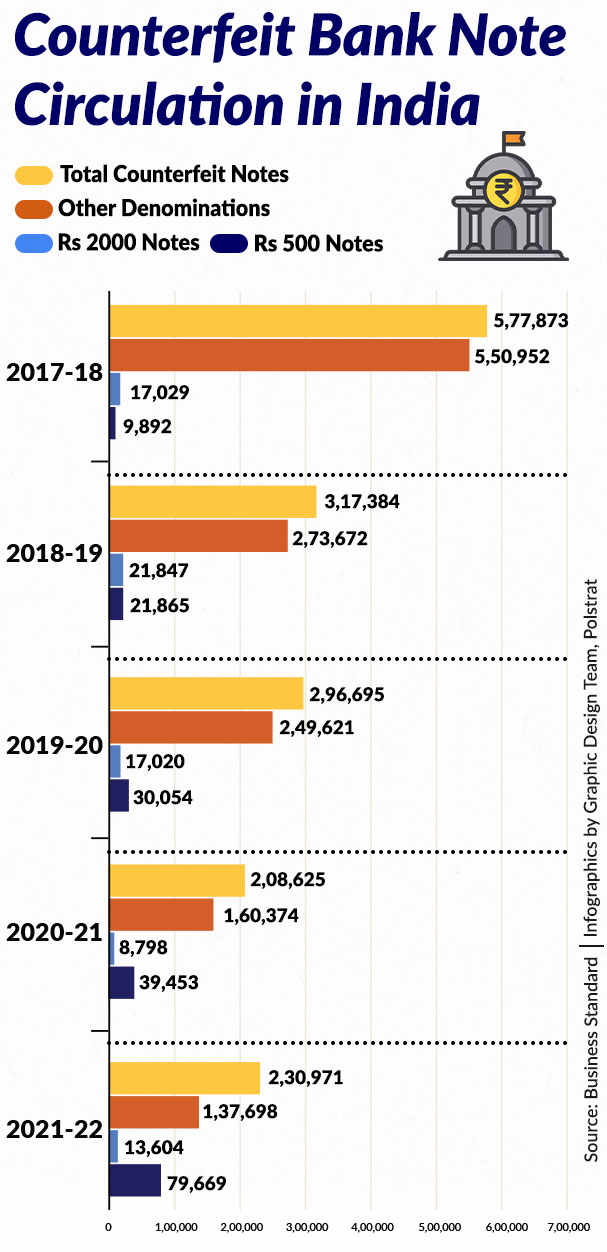

The Digital Rupee will also solve the issue of counterfeit bank note circulation in the country. While there has been a decline in the counterfeit currency note circulation in India from over 5.80 lakh counterfeit notes in the year 2017-18 to 2.30 lakh in 2021-22, a drop of more than 60 per cent, the damning impact of fake currency on the economy and individuals needs to be countered using innovation measures, one of which is digital currency.

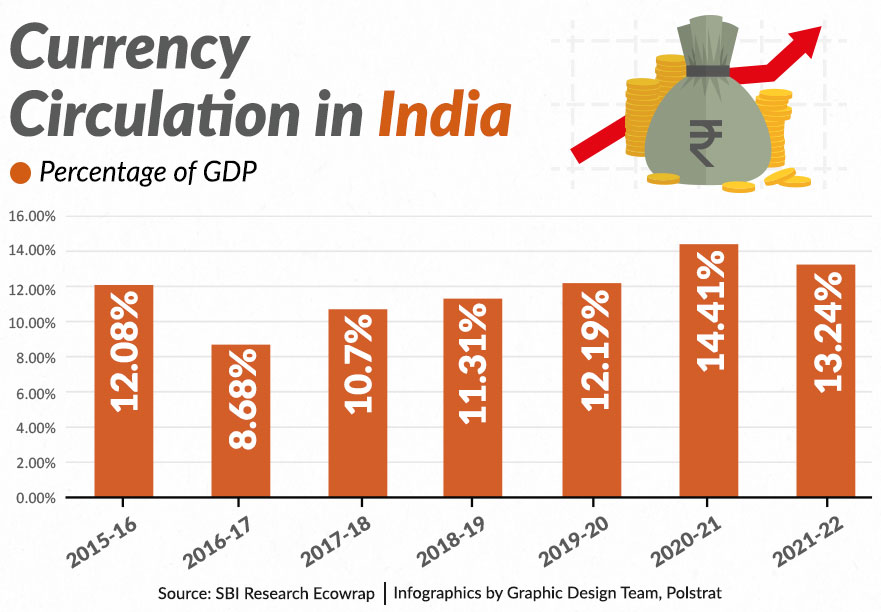

Currently, currency in circulation is accounted for at 13.24 per cent of the GDP of the country. If a large part of this fiat currency, in physical form right now, can be moved to Digital Rupee, it will bring huge savings to the RBI and the country in the form of cost reduction in maintaining physical currency. The expenses associated with maintaining paper money form a significant portion of the RBI’s account books. Damaged money further raises the expense of managing and processing fresh currency for the central bank. All of this can be decreased with the introduction of a controlled digital currency such as the Digital Rupee.

What is the Digital Rupee?

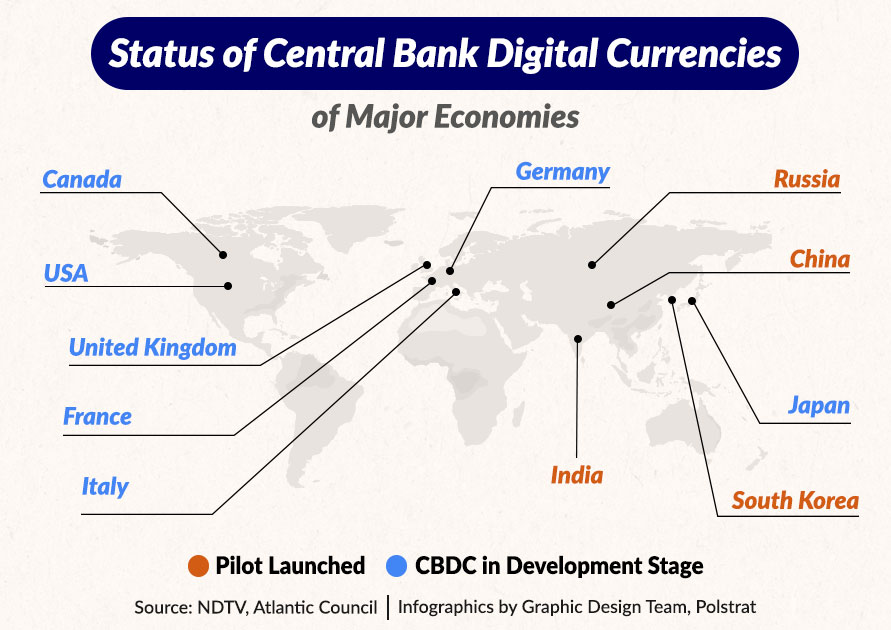

A Central Bank Digital Currency (CBDC) is a digital form of currency notes issued by the central bank of a country. Digital Rupee is the digital currency launched by India’s central bank, RBI, and is an electronic form of money that can be used in contactless transactions. It is essentially legal tender backed by the RBI and offers features similar to physical cash such as trust, safety, and settlement finality. It can be easily converted to other forms of money, like deposits with banks, but will not earn any interest (similar to how we use cash). As of December 2022, at least 11 countries are already using digital currencies (CBDC) in full measure with 17 others currently running it in the pilot stage. Data from the Atlantic Council indicates that more than 72 countries have a CBDC in the research and development stage..

The Indian government announced the launch of the Digital Rupee from Financial Year 2022-23 onwards during the presentation of the Union Budget 2022-23.

Flip to Digital Economy and Cross-Border Payments

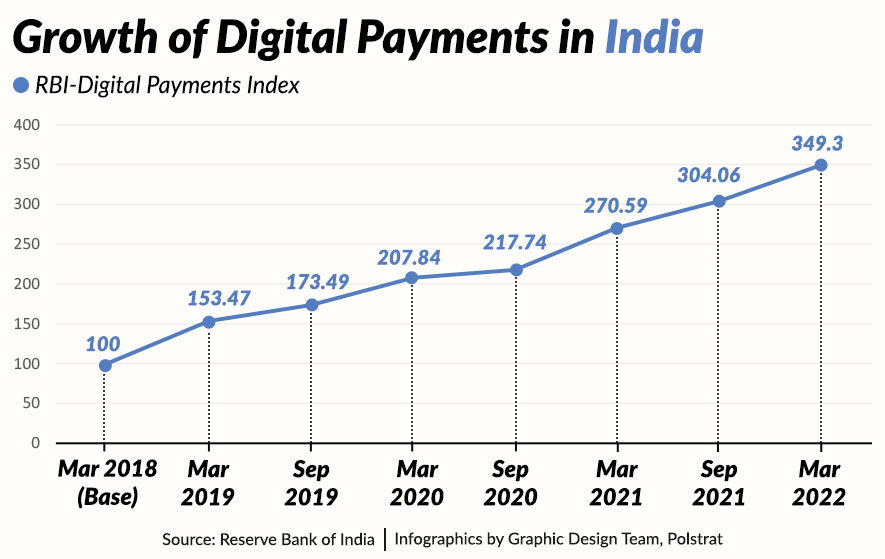

An increasing pace of digital transactions in India as established by the jump in RBI’s Digital Payments Index from a base of 100 in March 2018 to 349.30 in March 2022 clearly indicates the Indian economy’s appetite for digital forms of transactions. Further digitisation of payment systems through online transactions with Digital Rupee will boost the formalisation of the economy. The informal sector currently makes up close to 53 per cent of the Indian economy. Shifting paper-based currency to the Digital Rupee will help reduce the informal sector in the economy by introducing more transparency and efficiency to the payment structure.

The CBDC has the potential to enable more real-time and cost-effective globalisation of payment systems as it will be the currency which is transacted in real-time instead of bank balances and will eventually reduce the need for interbank settlements. Once digital currencies are made acceptable in other countries, cross border payment transactions will become easier by eliminating the need for an intermediary.

According to some experts, since digital currency will reduce the dependency on paper, the e-rupee can bring huge savings to the environment. However, many others doubt the incremental benefits of digital currency on the environment, given shifting to a digital currency will induce costs of online transactions, and thereby environmental costs of energy usage, electronic devices etc.

The Operational Framework

In India, the RBI has launched two forms of Digital Rupee – e₹-W, the wholesale Central Bank Digital Currency and e₹-R, the retail Central Bank Digital Currency. The wholesale e-rupee will be used by large financial institutions, including banks, large non-banking finance companies, and other big transaction institutions whereas the retail e-rupee is open for use for everyday transactions. The pilot initially covers four cities—Mumbai, New Delhi, Bengaluru, and Bhubaneswar —where customers and merchants will be able to use the digital rupee (e₹-R), or e-rupee, with four banks involved in the controlled launch of the digital currency. According to the RBI, the service will subsequently be extended to Ahmedabad, Gangtok, Guwahati, Hyderabad, Indore, Kochi, Lucknow, Patna, and Shimla as four more banks will join the pilot.

The e₹-R will be in the form of a digital token that represents legal tender and will be issued in the same denominations as paper currency and coins to be distributed through intermediaries, that is, banks. Users will be able to transact with e₹-R through a digital wallet offered by the participating banks and stored on mobile phones and devices.

The idea of a CBDC is inspired by cryptocurrencies such as Bitcoin, but differs from crypto assets which do not possess ‘legal tender’ status and are not issued by the state. The underlying technology in both forms of currencies – private cryptos such as Bitcoin and Ethereal and government backed digital currencies such as e-Rupee in India and eNaira in Nigeria – remains the same. The digital rupee is based on blockchain technology which came into the limelight with the popularity of cryptocurrencies. It is a tool now shunned by countries such as China and Egypt while readily adopted by other countries such as Denmark, France, and Germany in some form. Blockchain technology maintains a trail of transactions using the digital currency thereby eliminating the risk of duplicating a unit of currency.

Addressing Concerns

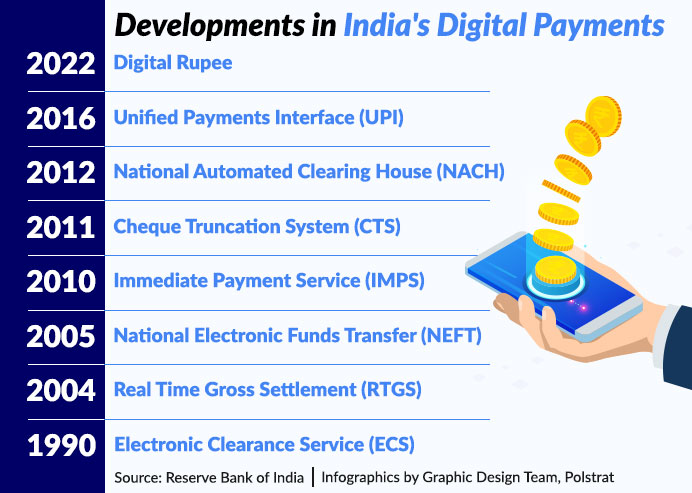

From the launch of Electronic Clearance Service (ECS) in the 1990s, one of the first forms of digital transactions in India, to UPI in 2016 and now the Digital Rupee in 2022, India has come a long way in using technology to revolutionise payments and online transaction systems. The first few weeks of launch of the e-rupee have witnessed a muted adoption of the digital fiat currency, for now only open to limited users in the pilot mode. Lack of trust is being cited as a major prohibiting factor in the adoption and acceptance of legal tender in digital form.

In a country where several households still find it difficult to trust banking systems with protecting and growing their savings, the adoption of a digital form of currency might be more difficult to accept. Risks of digital currencies range from reducing the need of banks to act as intermediaries and their ability to plough back funds into credit intermediation, elevated cyber security risks, vulnerability testing, and operational burden and costs for the central bank in managing CBDC. Several users have also expressed concerns in using the Digital Rupee as it reduces privacy relative to physical cash as the CBDC holdings could be tracked and accounted for. Lastly, data privacy threats and compromise of credentials in an environment where protection of personal data in all forms is gaining fast traction appears to have cut out the RBI and the government’s task in both reducing risks associated with the Digital Rupee and generating trust amongst the public for wider adoption as the e-rupee moves from pilot mode to full usage.