If COVID-19 had not struck India, the top seven real estate markets in India were to see the delivery of nearly 4.66 lakh units by end of 2020. Launched after 2013, many of the projects were in the final leg of completion. With almost zero construction activity in last few months due to the lockdown, the completion deadlines for almost all these projects has got extended.

The seven markets most affected are National Capital Region (NCR), Mumbai Metropolitan Region (MMR), Bengaluru, Pune, Kolkata, Hyderabad and Chennai.

Most state Real Estate Regulatory Authorities (RERA) have already given a 6-month extension to developers on previously committed timelines. However, homebuyers’ wait could run into several additional months for well-funded projects, and as much as 2 years for others. 2021 was to see completion of nearly 4.12 lakh units across the top 7 cities – 12% lower than in 2020. Most of these projects will probably also get delayed.

NCR, MMR & Bengaluru had completion of more than 1 lakh units each lined up in entire 2020 – then COVID-19 struck. Pune had 68,800 units lined up for completion, Kolkata 33,850 units & Hyderabad nearly 30,500 units; Chennai had least pending delivery at approx. 24,650 units. With most state RERAs giving developers a 6-month extension on deadlines, homebuyers’ wait gets longer. 2021 was to see completion of nearly 4.12 lakh units across top 7 cities. In 2020 & 2021 combined, NCR has the maximum units to be delivered at approx. 2.40 lakh. Unless labour shortage is addressed immediately, project deliveries will stutter going forward

“Homebuyers will have to adjust to new realities. As many as 4.66 lakh units were slated to be delivered in 2020 and another 4.12 lakh in 2021. Maximum completions (in both years) were to happen in NCR (approx. 2.40 lakh units). This region is set to witness more project delays over and above the backlog of over 2 lakh units already delayed in the region from before,” said Anuj Puri, Chairman of ANAROCK property consultants.

“The Government must intervene to address multiple challenges including labour shortage in top cities. Even if developers have the financial strength, it will still take a while for most of them to resume construction because lakhs of labourers have left cities and migrated back to their villages. Moreover, many of the top cities are still grappling with the virus.”

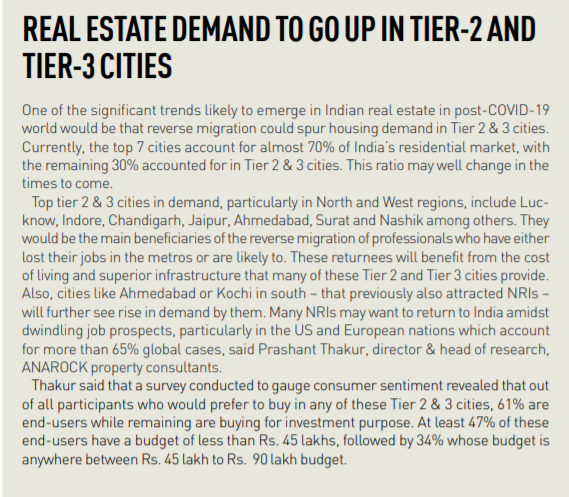

Projected Completions in 2020 and 2021

Prior to COVID-19, the top 7 cities were to see completion of over 8.78 lakh units in 2020 and 2021 combined. Of this total expected supply, nearly 4.66 lakh units were to be added in 2020 and the remaining 4.12 lakh units in 2021.

NCR was to see maximum completions in both years, of about 2.40 lakh units. Of this, 1.01 lakh units were to come up in 2020 and another 1.39 lakh units in 2021. MMR is second with nearly 2.10 lakh units expected to be delivered in two years, 1.07 lakh units in 2020 and nearly 1.03 lakh units in 2021. Bengaluru was expected to see delivery of nearly 1.51 lakh units in 2020 and 2021. This year the city was likely to see delivery of 1.01 lakh units while in the next year it was just half at nearly 50,000 units. Pune was to see completion of nearly 1.36 lakh units in both years, 69,000 in 2020 and 67,000 in 2021. Kolkata was next with nearly 59,000 units meant to be delivered in two years, 33,900 units in 2020 and nearly 25,100 units in 2021. Hyderabad was to see completion of more than 45,200 units in both years, 30,500 units in 2020 and another 14,700 units in 2021. Chennai had the least completions in both years, about 37,000 units. Of this, 24,650 units were to complete in 2020 while another 12,520 units in 2021.

Tarun Nangia is the host and producer of Policy & Politics.