Tourism stands as one of the world’s largest economic sectors, fostering job creation, driving exports, and promoting prosperity on a global scale. Its potential to contribute significantly to local economies is evident, particularly in a diverse country like India, celebrated for its landscapes, cuisines, heritage, adventure, wildlife, and rich culture. Over recent years, India has gained recognition as a prominent destination for both international and domestic travellers.

Recognizing tourism’s integral role in the economy, the Ministry of Tourism, Government of India, has undertaken various development initiatives. The importance of tourism statistics cannot be overstated in this context. Timely, comprehensive, accurate, and reliable statistics play a crucial role in shaping sound economic development policies. They serve as an essential ingredient for the formulation of government decisions and development plans.

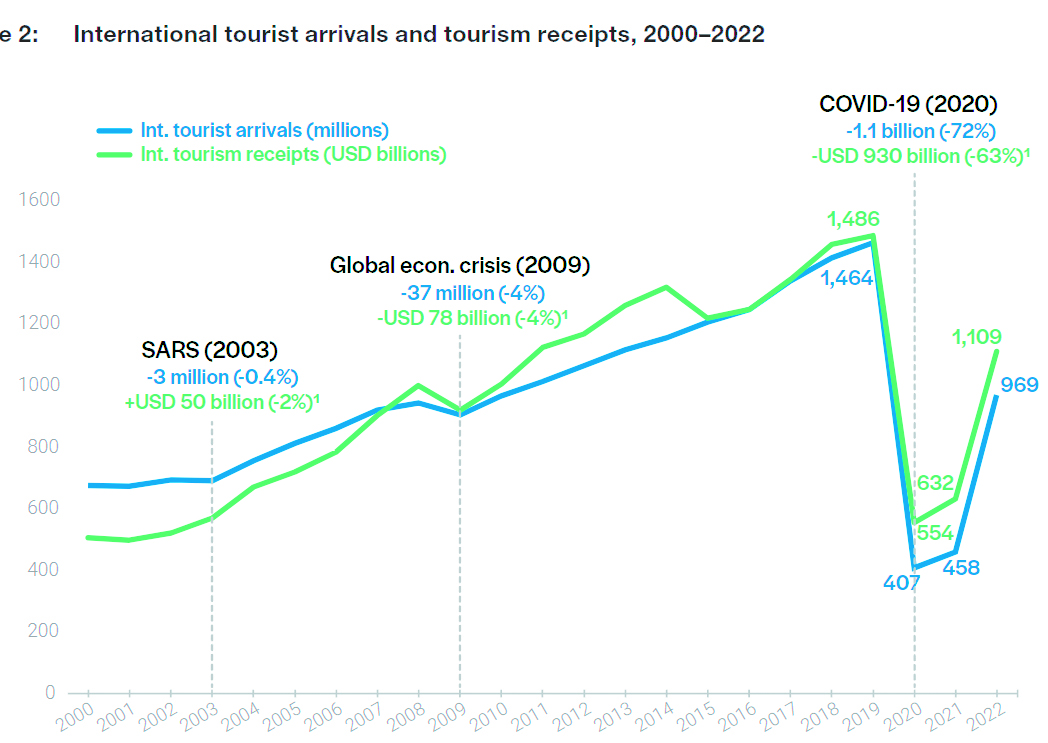

In 2023, the global number of international tourist arrivals witnessed an increase compared to the previous year. However, it remained below the 2019 figures, pre-dating the impact of the COVID-19 pandemic. The initial decline to approximately 407 million in the first year of the health crisis marked the lowest figure recorded since 1989. Subsequently, global inbound tourist arrivals exhibited robust signs of recovery in the following years, reaching just under 1.3 billion in 2023.

Tourism Statistics in India

In November 2023, the Foreign Tourist Arrivals (FTAs) reached 9,22,265, showcasing a notable increase from 7,89,330 recorded in November 2022. However, when compared to November 2019, which saw 10,92,440 FTAs, there was a decrease of -15.6%. The growth rate between November 2022 and November 2023 stood at 16.8%.

For the cumulative period of January to November 2023, the FTAs totalled 81,65,945. This marked a substantial growth of 50.0% compared to the same period in 2022, which recorded 54,44,490 FTAs. However, in comparison to the January to November period in 2019, with 97,03,957 FTAs, there was a decline of -15.8%. The data reflects the dynamic nature of international tourist arrivals over these specified periods.

Europe is the most popular destination for international tourism

Since 2005, Europe has consistently emerged as the leading global region in terms of attracting the highest number of international tourists. In 2022, there was a notable increase in inbound tourist arrivals to Europe compared to the previous year. However, the numbers had not yet reached the levels observed before the onset of the global COVID-19 pandemic.

Within Europe, Southern and Mediterranean Europe stood out as the most sought-after destination for international tourism, recording approximately 265 million arrivals in 2022. Despite the recovery, the region was still working towards matching the pre-pandemic levels of tourist activity. This underscores the resilience and enduring appeal of Europe as a key player in the global tourism landscape.

COVID-19 impact on the global travel and tourism market

The travel and tourism industries bore a significant brunt during the health crisis, facing substantial setbacks as countries globally imposed restrictions on non-essential travel to curb the spread of the virus. According to Statista’s Mobility Market Insights, the global travel and tourism market experienced a sharp contraction in revenue in 2020, witnessing a decline of approximately 55 per cent compared to the previous year.

In particular, segments such as cruises and package holidays reported some of the most substantial drops in revenue in 2020. The restrictions and uncertainties surrounding travel during the pandemic profoundly impacted these sectors, highlighting the challenges faced by industries heavily dependent on global mobility and tourism.

2020 became the worst year for the tourism sector

The year 2020 marked a profound global crisis with the advent of the COVID-19 pandemic, impacting health, society, and economies worldwide. Commencing in March 2020, the pandemic triggered an unparalleled disruption to the tourism sector, witnessing a substantial decline in international travel following widespread lockdowns and diminished demand due to extensive travel restrictions implemented to curb the virus’s spread.

International tourist arrivals, encompassing overnight visitors, plummeted drastically from 1.5 billion in 2019 to a mere 400 million in 2020, representing a staggering 72% drop. This unprecedented decline translated to 1.1 billion fewer international tourists, making 2020 the worst year on record.

The scale of this contraction far surpassed the 4% reduction witnessed during the global economic crisis in 2009, returning cross-border travel numbers to levels reminiscent of three decades ago.

In 2020, both international tourism receipts and total export revenues from tourism, inclusive of passenger transport, experienced a severe 63% decline. The financial impact amounted to a loss of USD 1.1 trillion. The implementation of various travel restrictions, including border closures, quarantines, curfews, and mandatory testing, was widespread across destinations.

These measures severely disrupted cross-border mobility, exacerbated by the absence of a COVID-19 vaccine. The lack of coordination among countries regarding health safety protocols and restrictions further contributed to the uncertainty and weakened demand. Tourism emerged as one of the sectors most profoundly affected by the pandemic, with businesses, employment, and livelihoods globally suffering severe consequences.

In 2023, international tourist arrivals worldwide displayed an increase across all regions compared to the previous year. However, with the exception of the Middle East, inbound arrivals remained below the figures reported in 2019, pre-dating the impact of the COVID-19 pandemic. Europe, overall, reported the highest volume of inbound travellers during this period, with around 700 million arrivals in 2023.

Economic impact of the pandemic

The impact of the COVID-19 pandemic on international tourism revenues has been significant. In 2020, export revenues from international tourism, which include international tourism receipts and passenger transport fares, saw a substantial decline from USD 1.7 trillion in 2019 to 0.6 trillion. This marked a staggering loss of USD 1.1 trillion, reflecting a 63% decline in real terms, measured in local currencies and constant prices.

While there was an 8% growth in revenues from international tourism in 2021, reaching USD 739 billion, it remained 60% below the levels recorded in 2019. These revenues encompass the ‘travel’ and ‘passenger transport’ items in the Balance of Payments.

With the reopening of many destinations in 2022, travel experienced a rebound, and revenues climbed to USD 1.3 trillion, reflecting a substantial 77% increase from 2021. However, despite this recovery, the figures remained 24% below the levels observed in 2019.

The cumulative loss in international tourism revenues is estimated at USD 2.5 trillion for the years 2020, 2021, and 2022. Specifically, international tourism receipts, which exclude passenger transport fares, followed a similar trajectory, dropping from USD 1.5 trillion in 2019 to USD 0.6 trillion in 2020, reflecting a 63% decline. Receipts remained 60% below pre-pandemic levels in 2021 and 26% in 2022.

Tourism in various regions

The impact of the pandemic on international tourist arrivals varied across regions. In 2020, Asia and the Pacific, being the first region affected by the pandemic and having stringent travel restrictions, experienced the largest relative decline, with an 84% decrease in international arrivals. This translated to about 300 million fewer arrivals compared to 2019.

Europe recorded a 68% decrease in arrivals in 2020, despite a brief revival in the summer. It suffered the most significant drop in absolute terms, with over 500 million fewer international tourists.

Arrivals in the Americas also declined by 68%, representing 150 million fewer international tourists. Both the Middle East and Africa saw a 73% decrease in arrivals.

All subregions worldwide witnessed substantial drops in arrivals ranging from 70% to 90%, except for Western Europe, North America, and the Caribbean, where the decline was less than 70% in 2020. Europe and the Americas saw a strong rebound in 2021.

In 2021, the Middle East and Europe recorded the best results by region compared to 2020, with arrivals up by 56% and 26%, respectively, although they remained almost 60% below 2019 levels.

The Americas saw a 17% increase in 2021 compared to 2020 but remained 63% below 2019 levels. Arrivals in Africa grew by 5% versus 2020 but were still 72% lower compared to 2019. In Asia and the Pacific, arrivals dropped 58% from 2020 levels and 93% compared to pre-pandemic values, as many destinations remained closed to non-essential travel.

By subregion, the Caribbean showed the best performance in 2021 relative to 2019, with international arrivals reaching 55% of pre-pandemic levels (-45% compared to 2019), and some island destinations even surpassing 2019 levels. Southern Mediterranean Europe also experienced a significant rebound.