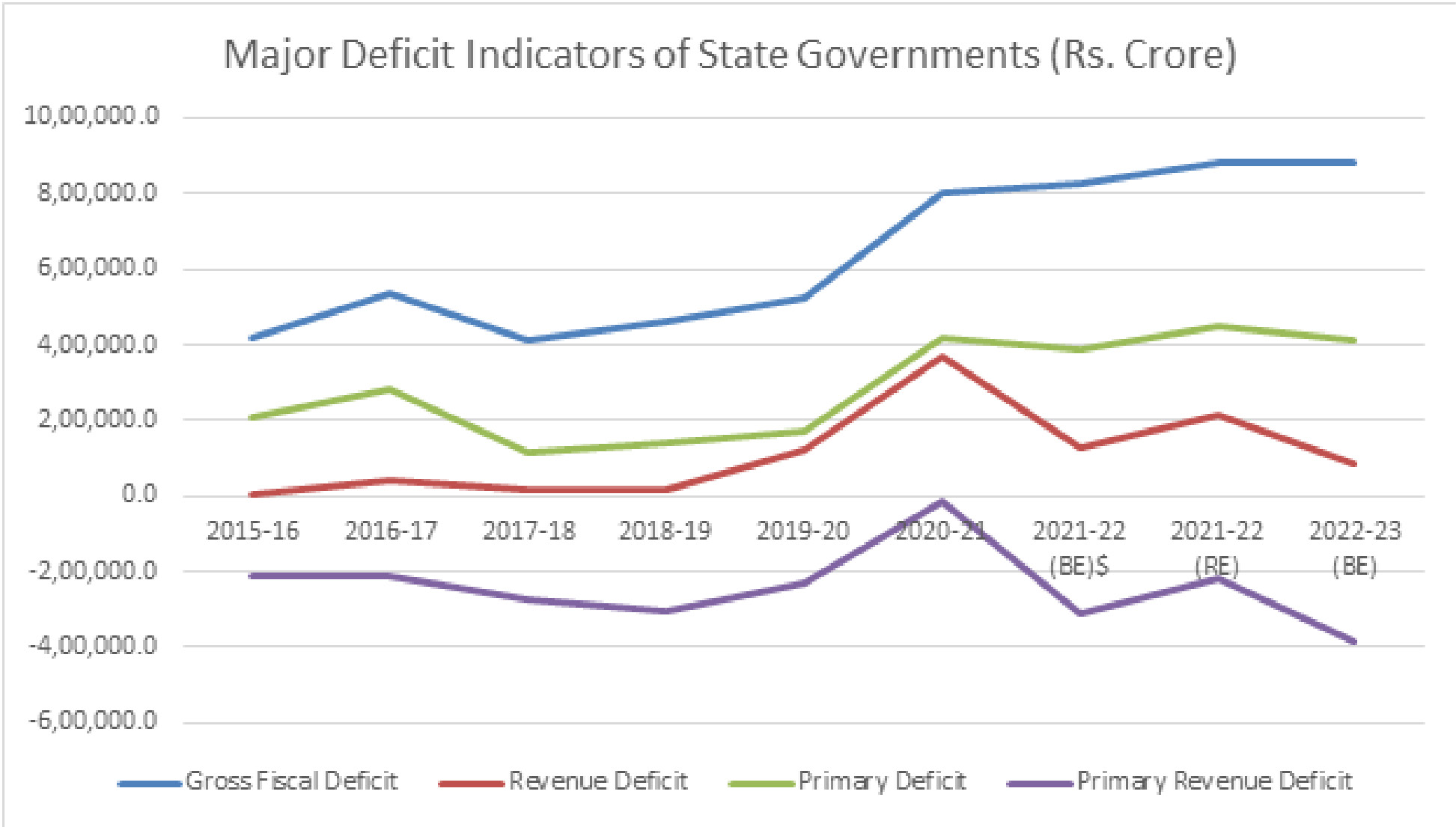

According to the RBI’s Report on State Finances (16 January 2023), for 2021-22, state governments have experienced reasonable uplift in their revenue receipts led by own tax and non-tax revenues and grants from the Centre. Nevertheless, unaudited data released by the CAG indicate lower revenue collections than in the revised estimate (RE). The grant component declined in 2021-22, and gradually over recent years, Revised Estimates (RE) often provide ambiguous signals about the health of State finances, as highlighted by the report.

For 2022-23 (RE), at the Central level, the budgeted fiscal deficit target is kept at 6.4% of GDP. Interestingly, for the Central Government, the revenue expenditure remains higher, thus putting pressure on finances from receipts side, for instance, revenue expenditure exceeded the budget estimates (BE) by Rs 2.6 lakh crore while capital expenditure fell short by Rs 21,972 crore, therefore, total expenditure has been uplifted by Rs 2.4 lakh crore.

For 2023-24, the Gross Fiscal Deficit (GFD) is budgeted at 5.9% of GDP. What is a matter of concern, despite the impressive and substantial growth of the (net) direct tax collection by 17% for this fiscal year (which is 83% of the revised target for the full financial year), there is some probability that the FY23 tax collection may not achieve the Revised Estimate (RE). The RE for the current fiscal has been increased by more than 10% to Rs 30.43 trillion, while the expected net collection could be between Rs 15-15.5 trillion. The Revenue Deficit (BE) in 2023-24 is kept at Rs 8,69,855 crore, which seems a bit optimistic. When the actuals in 2021-22 was Rs 10,31,021, and Revised Estimate (RE) in 2022-23 was 4.1%, the assumption that it would remain at 2.9% of GDP in 2023-24 seems rather more optimistic.

From the perspective of the state governments, the requirement of GST compensation is not uniform across various state governments. The states which are likely to be most adversely affected by the end of the compensation regime are Puducherry, Punjab, Delhi, Himachal Pradesh, Goa and Uttarakhand. On the other hand, the north-eastern states have been the biggest beneficiaries in the GST regime, recording a compound annual GST revenue growth rate of 27.5% since the implementation of the GST (2017-18 to 2022-23) as against 14.8% for all states.

Another issue is that the capital outlay of states recorded a robust growth of 31.7% in 2021-22. The capital outlay of the states registered a y-o-y growth of 0.9% in April-October 2022. This low capital outlay partly reflects the tendency to back-load expenditure in the latter half of the year. A state like Kerala has resorted towards additional revenue mobilization a string of tax increases and new cesses aimed at mopping up additional revenue in his Budget for the 2023-24 fiscal. Petrol, diesel and liquor will turn dearer after the announcement of a Social Security Cess on all three items. The state budget has further announced hikes in the one-time tax on motorcycles, cars and private service vehicles, the one-time cess on newly-registered motor vehicles, and the electricity duty applicable to commercial and industrial units.

There are certain caveats at various state-level, for instance, as noted by the fifteenth Finance Commission (FC), Himachal Pradesh has not done well in terms of GST collections. It needs to find innovative ways to increase both its own tax and non-tax revenues. Karnataka government has also taken steps for GST administration. Another matter of concern is that in its June 2022 report, the RBI had flagged three states viz. Kerala, Rajasthan and West Bengal as ‘fiscally vulnerable.’ A matter of further concern is that the total expenditure by eight state governments—namely Gujarat, Haryana, Karnataka, Kerala, Rajasthan, Telangana, Uttar Pradesh and West Bengal (this has been also highlighted by a ICICI Bank Research as well)—has not kept pace with the revenue collection. Within expenditure, their combined revenue expenditure as of January 2023 stands at INR 12.4tn or 71% of the full year target while capital expenditure has been lagging severely, having met only 36% of the full year target during April-January FY23. This trend has posed the question if such states would be able to meet fully their capital expenditure (capex) target.

Additionally, the state governments’ dependence on market borrowing has increased significantly following the recommendation of the Fourteenth Finance Commission to exclude States from the National Small Savings Fund (NSSF) financing facility (barring Delhi, Madhya Pradesh, Kerala and Arunachal Pradesh).

Since 2017-18, the share of market borrowings has increased rapidly and is budgeted to reach 78.1% in 2022-23. The share of market borrowings in total outstanding liabilities of the State governments is budgeted to increase in 2022-23. Furthermore, loans from the Centre are also expected to rise because of the 50-year interest-free loans being provided by the Centre under the scheme of Special Assistance to the States for Capital Investment. Moreover, while the outstanding liabilities of States have softened from their pandemic time peaks, debt consolidation at the individual State level merits serious attention and a “glide-path” needs to be set, as also emphasized by the RBI report.

Vipin Malik is Chairman & Mentor, Infomerics Ratings. Sankhanath Bandyopadhyay is Economist, Infomerics

Ratings.