Home loan interest rates hover at 6.85% – the lowest in decades. 66% of unsold homes are priced under Rs 80 lakh, and unheard-of deals are available and 5-year rental outgo for tenants living within city limits equals 27-52% of total property cost in peripheries of top cities.

At this point, does it make more sense to buy or rent a home? Many Indians who migrate to the urban centres ask themselves this question at some point. There are arguments for and against either option, but the debate has attained newer heights in the post-Covid-19 landscape.

Property supplements, real estate portals and others with ‘skin in the game’ espouse the benefits of buying – only to be dismissed by those who claim that in an uncertain job environment, homebuying sentiment cannot possibly be a serious compulsion.

Yet, homes are selling. As sales figures clearly indicate, people are quietly closing deals in a marketplace which has, counter-intuitively, been enabled by the Covid-19 crisis.

Covid-19 has polarised opinions on real estate like never before. As before, pro-renting advocates emphasise the arguments of flexibility, freedom of choice and reduced financial commitment. In the current time, they also add that renting is seen as the only choice for those who have lost their jobs or are in danger of doing so.

Curiously, there is almost no discussion about people whose jobs are secure, who have always wanted to own a home, and whose previous equivalence has now been eliminated by the pandemic. Many now choose not to face the future with such uncertainty again. If they were ambivalent about buying a home before, their minds are now made up, and they are acting.

While those who already own their homes in Covid-19 times are indeed fortunate, the pandemic also brings unique advantages for those seeking to secure the ultimate asset in the current time:

Pandemic deals: The lockdowns have impacted sales and developers want to make up for the lost time and clear inventory. It is clear that the unheard-of deals available now are because of pandemic market conditions. As such, they will vanish once the crisis blows over.

Calculations favour buying: The buyers on the market now have done their homework. The 5-year rental outgo for city living amounts to 27-52% of the cost of a home in the suburbs of MMR, NCR and Bengaluru. This is a strong financial rationale for suburban homeownership *

The need for autonomy: In the current context, people need homes that they can adapt to their requirements – and rented homes don’t offer this flexibility. From a workfrom-home perspective, the onus is no longer on small rented homes in the city centres whose landlords will not permit to be altered – it is on larger homes which can be adapted at a will.

Rock-bottom home loan rates: Homebuyers were hoping for lower home loan interest rates. The economic compulsions of pandemicreduced consumption have pressed interest rates down to as low as 6.85% – the best rates in decades. The repo rate to which home loan rates are linked is at a 20- year low:

The price is right: While inferior projects have seen distress-related price correction, it is now clear that developers of quality housing will hold on to prices that are already trimmed as low as they can get. When prices do not reduce even in a pandemic slowdown, they are evidently at their lowest best. Average residential real estate prices across the top 7 cities have been rangebound for the past 5-6 years, and 66% of unsold homes are priced under Rs 80 lakh.*

No new launches: New launches increase supply and thereby cause prices to reduce. However, there will be very few new project launches now as developers will focus on clearing existing inventory. The market will thus attain equilibrium in a few quarters and then become more developerfavouring. This means that prices will harden.

Hard asset in uncertain times: The Covid-19 pandemic has caused everyone to take a hard look at what they can fall back on when things go south. An owned home is freedom from rent, while rent is a recurring expense which does nothing but push the stop-watch ahead a month at a time.

Investment ratio – nale: Living on rent does not help to create an asset, while homeownership does. Simultaneously, other popular investment asset classes such as stocks and gold are volatile and unpredictable in pandemic times. Housing retains its intrinsic value in uncertain times and eventually appreciates when times improve. Also, home loans come with attractive tax benefits. Rental housing doesn›t.

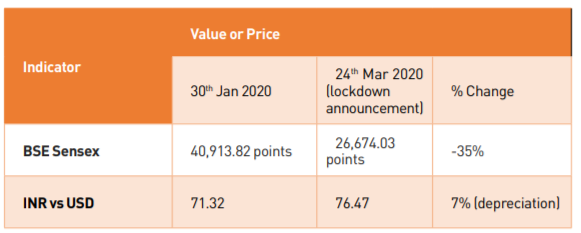

The first Covid-19 case in India was recorded on 30th Jan 2020. Since then, many investment indicators depicted a sharp decline for the next few months, eroding a significant amount of invested capital.

Those who are buying now homes are aware of these benefits, many of which are strictly time-bound. The Covid-19 pandemic is a once-in-a-lifetime event and the advantages it brings for homebuyers will not be repeated. The renting population will not thin out – it is clear that the pandemic has had many financial fatalities. For many, renting may be the only choice.

However, those with options are now playing for the long-term. Regardless of what else may happen in the future, home and hearth need to be secured while the odds are so unprecedentedly favourable. *

Considering the total annual rental outgo for 5 years + 3.5% annual rental appreciation. E.g. in MMR, the average monthly rental outgo in city-limit areas is Rs 45,800. For five years, this equals nearly Rs 28.66 lakh (including standard rental escalation for this period). This is almost 52% of the total average cost of a property in MMR›s peripheral areas.

Santhosh Kumar is Vice Chairman of ANAROCK.